Financials

Financials

Full Year Financial Statements And Dividend Announcement 2025

Financials ArchiveCondensed interim consolidated statement of comprehensive income

Condensed interim consolidated statement of financial position

Review of Performance

Profit or Loss

2H 2025 vs. 2H 2024

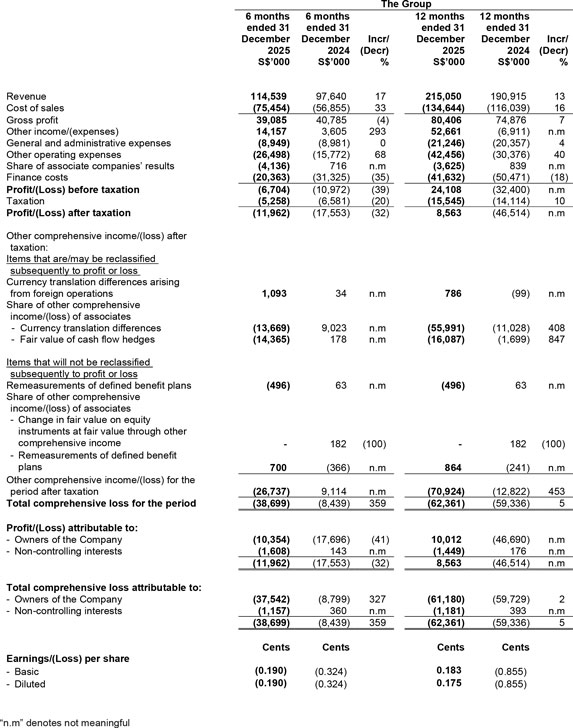

The Group reported revenue of S$114.5 million in 2H 2025, up 17.3% year-on-year compared with 2H 2024's S$97.6 million. Growth was driven by higher contributions from the industrial parks segment, supported by increased leased area and improved rental yields, higher utility revenue from tenants and new hotels in Bintan Resorts, stronger ferry and tourism-related performance, and new contributions from the new business segment on sales and distribution of coconut-related products.

The Group's cost of sales increased from S$56.9 million in 2H 2024 to S$75.5 million in 2H 2025, primarily due to higher natural gas costs and the inclusion of cost of sales from the new business segment. The cost of sales- to-revenue ratio rose to 0.66 in 2H 2025, from 0.58 in 2H 2024. Consequently, the Group's gross profit decreased from S$40.8 million in 2H 2024 to S$39.1 million in 2H 2025.

The Group's other income increased to S$14.2 million in 2H 2025, from S$3.6 million in 2H 2024. The increase was primarily attributable to insurance claims, receipts of amounts previously written off, gains from the assignment of receivables, and the write-off of unclaimed refundable membership deposits.

The Group's general and administrative expenses were S$8.9 million in 2H 2025, comparable to S$9.0 million in 2H 2024.

The Group's other operating expenses increased to S$26.5 million in 2H 2025, from S$15.8 million in 2H 2024, primarily due to a goodwill write-off of S$4.0 million, depreciation on the fair value uplift of property, plant and equipment, and the inclusion of operating expenses from the new business segment.

The Group reported a loss of S$4.1 million from its associate companies in 2H 2025, compared with a profit of S$0.7 million in 2H 2024, mainly due to a S$2.6 million loss from PT IMAS and a higher loss from Regent arising from the deconsolidation of its subsidiary.

The Group's finance costs were S$20.4 million, lower than the 2H 2024 level of S$31.3 million. The 2H 2024 figure included a one-time non-cash write-off of S$8.4 million for unamortised transaction costs incurred in refinancing.

The Group's tax expenses decreased to S$5.3 million in 2H 2025, compared with S$6.6 million in 2H 2024.

The Group reported a net loss attributable to owners of the Company of S$10.4 million in 2H 2025, compared with a net loss of S$17.7 million in 2H 2024.

12 Months 2025 (FY2025) vs. 12 Months 2024 (FY2024)

The Group reported revenue of S$215.1 million for FY2025, up 12.7% compared to S$190.9 million in FY2024. The increase was mainly driven by higher contributions from the industrial parks segment, supported by increased leased areas from newly completed factory units and improved rental yields, resulting in stronger rental, related income, and utilities revenue. Revenue from ferry services and tourism-related activities also improved in line with higher tourist arrivals, while the Group's new business segment on coconut-related products contributed S$6.0 million.

The Group's cost of sales increased from S$116.0 million in FY2024 to S$134.6 million in FY2025, primarily due to higher gas generation costs and the inclusion of cost of sales from the new business segment. The cost of sales-to-revenue ratio rose to 0.63 in FY2025, from 0.61 in FY2024. In line with higher revenue, the Group's gross profit increased from S$74.9 million in FY2024 to S$80.4 million in FY2025.

The Group's other income was S$52.7 million in FY2025, compared to other expenses of S$6.9 million in FY2024. This was mainly due to a foreign exchange gain of S$33.5 million in FY2025, compared to a foreign exchange loss of S$11.5 million in FY2024, from the depreciation of the US dollar against the Singapore dollar on USD- denominated liabilities, insurance claims, receipts of amounts previously written off, gains from the assignment of receivables, and the write-off of unclaimed refundable membership deposits.

The Group's “general and administrative expenses” were S$21.2 million, compared to S$20.4 million in FY2024. The increase was mainly due to higher manpower-related expenses and business development expenses.

The Group's other operating expenses increased to S$42.5 million in FY2025, from S$30.4 million in FY2024, primarily due to a goodwill write-off of S$4.0 million, depreciation on the fair value uplift of property, plant and equipment, higher depreciation and the inclusion of operating expenses from the new business segment.

The Group reported a loss of S$3.6 million from its associate companies in FY2025, compared with a profit of S$0.8 million in FY2024. At the PT IMAS level, the company reported a profit for FY2025, including fair value gains on investment properties. However, as the Group accounts for investment properties under the cost method rather than the fair value model, these gains were not recognised. After this adjustment, the Group's share of PT IMAS's results was a loss of S$2.3 million, compared with a profit of S$0.9 million in FY2024.

Regent reported higher losses in FY2025, mainly due to the deconsolidation of subsidiaries and one-time expenses related to a new acquisition. As a result, the Group's share of Regent's results amounted to a higher loss of S$1.9 million.

The Group's finance costs decreased to S$41.6 million in FY2025, compared with S$50.5 million in FY2024. The FY2024 figure included a one-time, non-cash write-off of S$8.4 million for unamortised transaction costs incurred in refinancing.

The Group's tax expenses increased to S$15.5 million in FY2025, from S$14.1 million in FY2024, primarily due to higher tax on rental and related revenue.

The Group reported a net profit attributable to owners of the Company of S$10.0 million in FY2025, compared with a net loss of S$46.7 million in FY2024.

Financial position

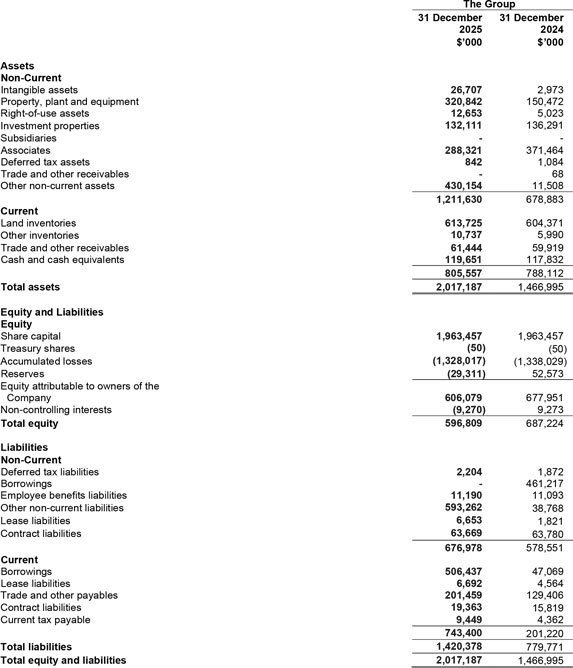

As of 31 December 2025, the Group's total assets were S$2,017.2 million, compared to S$1,467.0 million at the end of the previous year.

Intangible assets increased by S$23.7 million, mainly due to the recognition of goodwill arising from the acquisition of PT Bionesia Organic Foods. Property, plant, and equipment increased by S$170.3 million, primarily due to capital expenditures on buildings, infrastructure, and construction of new factories and the new power plant, partially offset by depreciation. Right-of-use assets increased by S$7.7 million, relating to additional utilities plant and machinery, while investment properties decreased by S$4.2 million due to depreciation.

The Group's interests in associates decreased by S$83.2 million, mainly due to the Group's share of PT IMAS's other comprehensive loss and reserves of S$81.9 million, which included a translation loss of S$58.0 million arising from the conversion of its financial statements from Indonesian Rupiah to Singapore Dollar, following the significant weakening of the Rupiah as of 31 December 2025.

Other non-current assets increased by S$418.7 million, mainly due to advances and deposits of S$421.2 million made for the Group's investment in new power plants, partially offset by a decrease in other receivables.

The Group's trade receivables increased by S$6.7 million, which is in line with higher revenue. Other receivables decreased by S$4.7 million, due to repayments of S$7.6 million owing from related parties, partially offset by advances paid to contractors for the construction of new industrial factories, the development of the airport project, the construction of resort-related facilities, and the Solar PV project.

As of 31 December 2025, the Group's total liabilities were S$1,420.4 million, compared to S$779.8 million at the previous year's end.

The Group's borrowings decreased by S$1.9 million due to loan repayments and the impact of foreign exchange translation on the US outstanding amounts, where the USD has depreciated against the Singapore dollar.

The Group's trade and other payables increased by S$72.1 million, mainly due to (i) amounts payable to contractors and suppliers for the construction of new factories in the Group's industrial parks and ongoing development in Bintan Resort, (ii) the consolidation of PT Bionesia Organic Foods, and (iii) higher rental and electricity deposits received from tenants of the new industrial park.

The Group's other non-current liabilities increased by S$554.5 million, mainly due to S$501.8 million advances received from investors intending to participate in the Group's investment in new power plants and the consolidation of PT Bionesia Organic Foods of S$5.5 million.

The Group's lease liabilities increased by S$6.9 million, primarily due to lease liabilities recognised for additional utilities plant and machinery, partially offset by repayments of the principal portion of existing lease liabilities. The Group's contract liabilities increased by S$3.4 million, mainly due to higher rental payments received in advance from industrial park tenants and advances received from travel agents for ferry services and tour packages to Bintan Resorts.

Cash Flow

For the year under review, the net cash inflow generated from operating activities was S$169.1 million, compared to the net cash outflow of S$39.4 million used in the previous year. The net cash inflow from operating activities was primarily driven by higher advances from the investor intending to participate in the Group's investment in new power plants and lower income tax payments during the current year.

The Group recorded a net cash outflow of S$177.8 million from investing activities, compared to S$81.7 million in the prior year. The higher outflow was mainly due to capital expenditure incurred for the development of new power plants, partially offset by lower construction expenditure on new factories in the industrial parks and reduced new investments in the current year.

The Group recorded a net cash inflow of S$11.3 million from financing activities, compared to S$128.2 million in the prior year. The lower net cash inflow in the current year was mainly due to smaller drawdowns from the facilities, reduced net borrowings, and the repayment of the principal portion of lease liabilities.

The Group's cash and cash equivalents in the statement of cash flow were S$100.1 million as of 31 December 2025, compared with S$97.7 million as of 31 December 2024.

Liquidity and financial resources

For the financial period ended 31 December 2025, the Group's working capital was mainly financed by internal resources generated from the operation, whilst the Group's capital expenditure in relation to the construction of new factories, expansion of the industrial parks and new investment/development was financed by advance lease payments from the tenants and bank borrowings. As of 31 December 2025, the cash and cash equivalents in the statement of financial position were S$119.7 million, which increased by 1.6% compared to S$117.8 million as of 31 December 2024. The Group's current ratio was approximately 1.1 times (31 December 2024 - 3.9 times). The decrease in the current ratio was primarily attributable to the reclassification of borrowings from non-current to current liabilities following a non-compliance with certain financial covenants.

As of 31 December 2025, the Group's borrowings were S$506.4 million. Borrowings due within one year were S$506.4 million (31 December 2024 - S$47.1 million), and borrowings due after one year are reclassified to the current portion (31 December 2024 - S$461.2 million). The increase in borrowings due within one year was primarily attributable to the reclassification of borrowings from non-current to current liabilities following a non- compliance with certain financial covenants.

The Group's borrowings were denominated in Singapore and United States dollars, with interest rates ranging from 3.76% to 8.10%. The Group's total debts, including lease liabilities, were S$519.8 million (31 December 2024 - S$514.7 million). As of 31 December 2025, the Group's gearing ratio was 0.9 times (31 December 2024 - 0.7 times), which was calculated on the Group's total debts to total shareholders' equity (including non-controlling interests). The increase was primarily due to lower total shareholders' equity.

Commentary On Current Year Prospects

The Group aims to capitalise on its recent successes in securing new tenants and expanding leased areas by constructing committed new factory units. It is now driving the next stage of growth through strategic developments, including logistics centres, initiatives targeting the expanding digital industries, and a new power plant to increase capacity and support growth. With these initiatives, the Group is confident that its industrial park and utilities segments will remain key drivers of profitability.

Tourist arrivals climbed by 23% for the full year, supported by major sporting and large-scale events, as well as the inaugural multi-dimensional festival integrating music, wellness, culture, and digital engagement, headlined by international DJs and attracting over 4,000 attendees in a single night. The Group continues to build on these initiatives and is focused on new developments and enhanced offerings, aiming to surpass one million tourist arrivals by the end of 2026.

The Group is also in the process of securing land sales from investors planning new tourism developments in Bintan Resorts. It is hopeful that these projects will materialise, further strengthening Bintan Resorts' position as a preferred tourism destination.